Suez and Panama Canal disruptions threaten global trade and development. The disruptions are straining supply chains, driving up costs, and reshaping global trade patterns, with vulnerable economies hit hardest, according to the latest UNCTAD analysis.

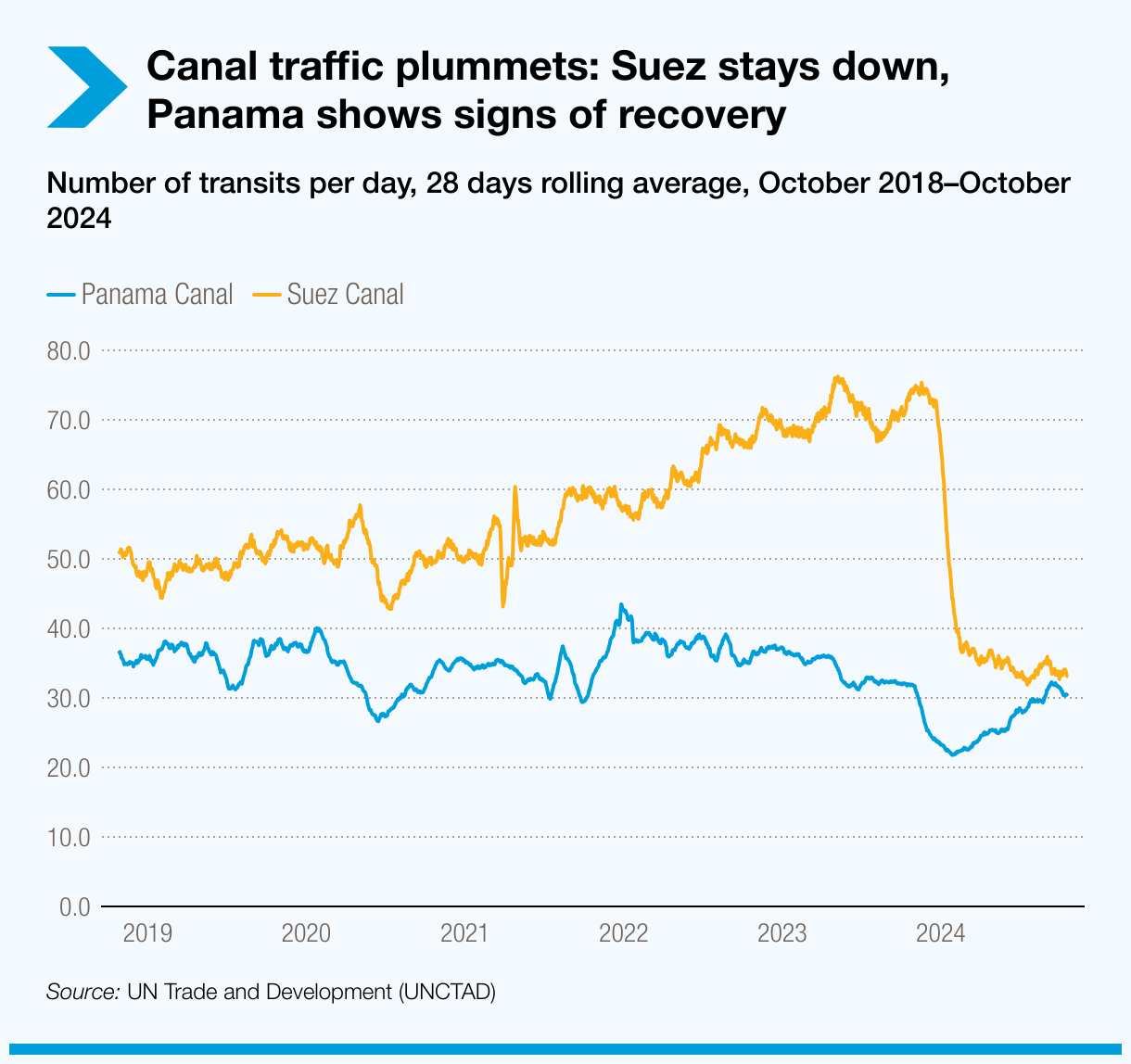

Canal traffic plumments: Suez stay down, Panama shows signs of recovery.

Global trade is facing significant disruptions as two of the world’s most vital maritime chokepoints – the Suez Canal and the Panama Canal – experience severe challenges driven by geopolitical tensions and climate-related risks.

In addition to straining global supply chains and undermining economic growth, these disruptions are driving up costs, reshaping trade patterns, upending the flow of energy and food supplies and threatening to exacerbate food security risks, especially in vulnerable economies.

Canal traffic plummets

The number of ships transiting through the Suez Canal hit rock bottom. The latest available data shows that by mid-October 2024, the average of 33 transits per day was 57% below its previous peak, 55% lower than one year ago and just 4% above the lowest recorded four-week average.

In contrast, Panama Canal traffic is showing signs of recovery. By mid-October 2024, the four-week average of 30 transits per day was 30% below the previous peak and only 4% lower than one year ago. Importantly, it was already 40% above the lowest level of transits recorded in early 2024.

Rerouting vessel capacity around Africa’s Cape of Good Hope has surged by 89%. While this keeps goods moving, it adds significantly to costs, delays and carbon emissions.

For example, a typical large container ship carrying 20,000–24,000 TEUs on the Far East-Europe route incurs an additional US$400,000 in emissions costs per voyage under the European Union’s Emissions Trading System (ETS) when diverting around Africa instead of using the Suez Canal.

Longer routes, higher costs

Longer routes have led to increased port congestion, fuel consumption, crew wages, insurance premiums and piracy risks, all while raising overall costs and greenhouse gas emissions.

Global ton-miles rose by 4.2% in 2023, further straining supply chains. By mid-2024, rerouting away from the Red Sea and Panama Canal increased global vessel demand by 3% and container ship demand by 12%.

Port hubs like Singapore and major Mediterranean ports are struggling with rising demand for transshipment services, adding to global congestion and delays.

Vulnerable economies hit hardest

Small island developing States (SIDS) and least developed countries (LDCs) are bearing the brunt of these disruptions.

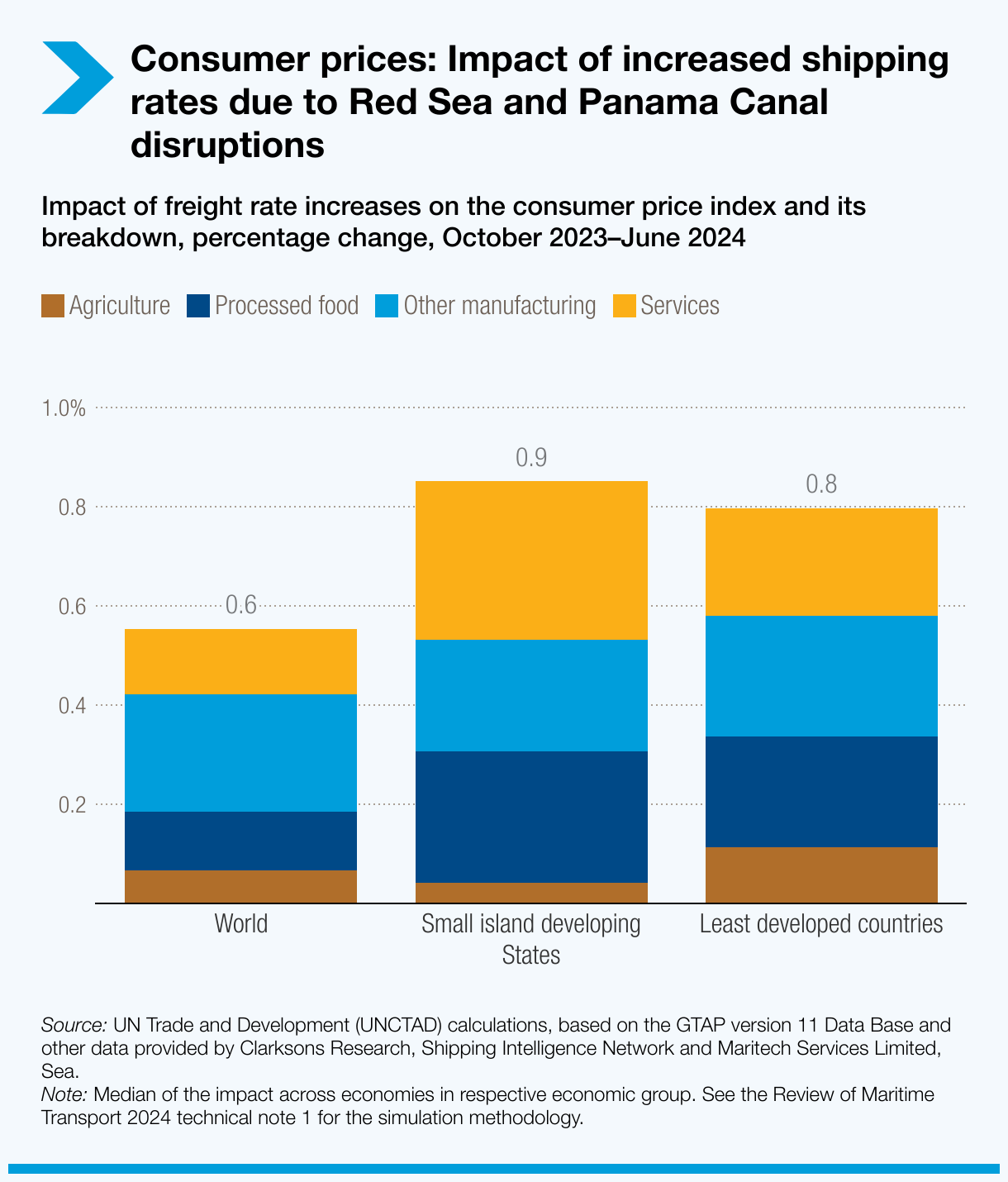

If the increase in container freight rates observed between October 2023 and June 2024 – driven by the Red Sea crisis and Panama Canal disruptions – continues through the end of 2025, global consumer prices could rise by 0.6% by late 2025.

SIDS would be the hardest hit, potentially facing a 0.9% increase, with processed food prices rising by 1.3%. These vulnerable economies, which rely heavily on shipping for essential imports, have seen their maritime connectivity decline by 9% over the past decade, leaving them ten times less connected to global shipping networks compared to non-SIDS countries.

Energy supplies are also at risk, as disruptions in key maritime routes affect the transportation of oil, gas and other critical energy commodities.

Swift action needed to mitigate global chokepoint vulnerabilities

In response to these growing challenges, UN Trade and Development’s (UNCTAD) Review of Maritime Transport 2024 calls for swift and coordinated action to safeguard global trade and mitigate the effects of these chokepoint vulnerabilities.

The organization emphasizes the need to:

- Strengthen international cooperation and enhance monitoring systems to ensure well-functioning shipping routes, provide early warnings and enable the rapid, efficient rerouting of vessels.

- Diversify shipping routes and support regional trade initiatives to reduce dependency on long-distance routes and boost intraregional trade flows.

- Invest urgently in resilient infrastructure at key chokepoints to minimize the impact of climate risks and conflicts.

- The challenges of the Suez and Panama canals highlight the fragility of global supply chains to disruptions, including those caused by mounting climate and geopolitical risks.